If you own property along the Texas Gulf Coast, you already know that windstorm insurance is not optional; it is essential. But what actually drives the cost of a standalone windstorm policy? From the age of your roof to your distance from the shoreline, multiple factors combine to determine the premium you pay each year. Understanding these variables can help you make smarter decisions, reduce unnecessary costs, and ensure you have adequate protection before the next hurricane season. This guide breaks down every major factor that influences windstorm insurance premiums in high-risk coastal areas like Texas City, Galveston, and surrounding communities.

What Is Standalone Windstorm Insurance?

Windstorm insurance is a specialized policy that covers property damage caused by high winds, including hurricanes, tropical storms, tornadoes, and severe thunderstorms. In many coastal Texas counties, standard homeowners insurance policies exclude wind and hail damage entirely, which means a separate windstorm policy is required for complete protection.

As Brad Spurgeon Insurance Agency explains, windstorm coverage typically pays for structural repairs, personal property replacement, loss of rental income, and additional living expenses if your home becomes uninhabitable. It does not cover flood damage, which requires a separate flood insurance policy.

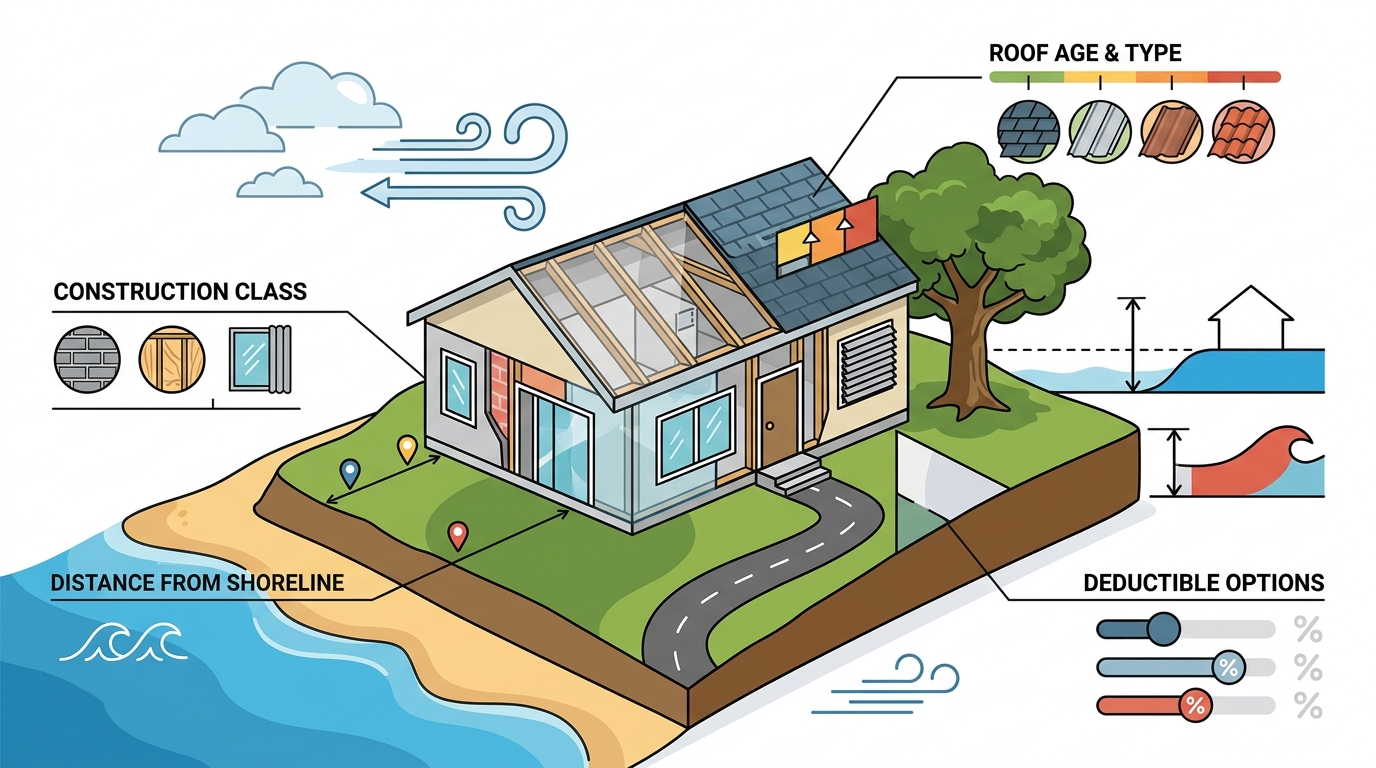

Location and Proximity to the Coast

Geographic location is the single largest factor affecting your windstorm premium. Properties closer to the coastline face greater exposure to hurricane-force winds, and insurers price that risk accordingly. According to TWIA, premiums are calculated based on standard rating factors including amount of insurance, type of construction, and deductible amount.

In Texas, TWIA-eligible counties include 14 directly coastal counties plus parts of Harris County east of Highway 146. Homeowners in cities like Texas City, Galveston Island, and Tiki Island should expect higher base rates than those further inland. Brad Spurgeon Insurance Agency offers windstorm insurance specifically tailored for these high-risk zones.

Construction Type and Building Codes

How your home was built plays a major role in premium calculations. A WPI-8 certificate is a windstorm inspection document that verifies a property meets the Texas Department of Insurance building code requirements. Without it, obtaining coverage may be difficult or impossible in designated coastal areas.

Homes built to modern wind-resistant standards, such as those meeting International Residential Code (IRC) specifications, can qualify for significant premium discounts. According to a 2025 cost analysis, homes certified under wind-resistant codes may earn discounts of up to 26%. Features like reinforced roof-to-wall connections, impact-resistant windows, and hip roofs all contribute to lower risk scores.

| Factor | Higher Premium | Lower Premium |

|---|---|---|

| Roof Shape | Gable roof | Hip roof |

| Roof Attachment | Toe-nailed connections | Hurricane straps/clips |

| Windows | Standard glass | Impact-resistant glass |

| Building Code Era | Pre-2002 construction | Post-2002 code-compliant |

| Exterior Walls | Wood frame only | Concrete block or masonry |

Deductible Choices and Coverage Limits

A deductible is the amount you pay out of pocket before your insurance kicks in. Windstorm policies in Texas typically use percentage-based deductibles rather than flat-dollar amounts, usually ranging from 1% to 5% of your dwelling coverage limit. Choosing a higher deductible, such as 5%, will lower your annual premium but increases your financial exposure when a claim occurs.

Coverage limits also directly affect cost. The more coverage you carry, the higher your premium. As of 2024, TWIA provides residential coverage up to a maximum limit of $1,773,000. Adjusting your policy limit to accurately reflect your home's replacement cost, rather than over-insuring or under-insuring, is one of the smartest ways to manage your premium. Learn more about why replacement cost coverage matters.

Roof Condition and Home Age

Your roof is the first line of defense against a windstorm, and insurers know it. A well-maintained or recently replaced roof made from impact-resistant materials can meaningfully reduce your premium. Conversely, an aging roof with missing shingles or outdated materials signals higher risk.

Home Age Matters

Newer homes built to current windstorm codes typically cost less to insure than older properties. If you have an older home, investing in retrofits like hurricane straps or a code-compliant roof replacement can help offset higher premiums. Brad Spurgeon Insurance Agency has helped homeowners across communities from League City to Galveston Island find affordable coverage for both new and aging properties.

Roof Inspections and WPI-8 Certificates

In designated coastal areas, a windstorm inspection is often required before a policy can be written. Properties that pass inspection and receive a WPI-8 certificate demonstrate compliance with building standards, which directly translates to premium credits.

TWIA vs. Private Market Windstorm Insurance

The Texas Windstorm Insurance Association (TWIA) is a state-created insurer of last resort for property owners who cannot obtain wind and hail coverage in the private market. For the past 20 years, TWIA was the only option for windstorm insurance on the Gulf Coast. Today, private market alternatives are increasingly available and sometimes offer lower premiums or broader coverage terms.

Cost Comparison

The average TWIA policy costs approximately $2,480 per year, according to Insurify. Private carriers, including surplus line companies like Lloyd's of London, may offer competitive or lower pricing depending on your property's risk profile. One key difference: TWIA does not use credit scoring when setting premiums, while some private insurers may factor it in.

Which Is Right for You?

The best choice depends on your property's characteristics, location, and personal preferences. An independent agent can compare both options side by side. Brad Spurgeon Insurance Agency now offers windstorm coverage with two private companies in addition to TWIA policies, giving clients more flexibility.

Practical Ways to Lower Your Premium

While you cannot change your property's location, several actionable steps can reduce your windstorm insurance costs:

- Retrofit to code: Adding hurricane straps, impact-resistant windows, or a new roof can qualify you for discounts of up to 26%.

- Choose a higher deductible: Opting for a 2% to 5% deductible instead of 1% lowers your annual premium significantly.

- Shop multiple providers: Comparing TWIA and private market options ensures you find the best rate. Request a quote from Brad Spurgeon Insurance Agency to start comparing.

- Bundle policies: Some carriers offer discounts when you pair windstorm coverage with home insurance or flood insurance.

- Maintain your roof: Regular inspections and prompt repairs prevent premium increases at renewal.

Key Takeaways

- Windstorm insurance is a specialized policy covering wind and hail damage, separate from standard homeowners insurance in coastal Texas.

- Proximity to the coast is the biggest premium driver; properties in TWIA-eligible counties pay more.

- Construction type, building code compliance, and WPI-8 certification directly affect your rate.

- Percentage-based deductibles (1% to 5%) are standard; higher deductibles reduce premiums.

- The average TWIA policy costs around $2,480 per year, but private market alternatives may offer savings.

- Roof condition, age, and materials are critical factors insurers evaluate.

- An independent agent can compare TWIA and private options to find the best fit for your property.

Frequently Asked Questions

What is windstorm insurance?

Windstorm insurance is a specialty type of property and casualty insurance that covers damage caused by wind or hail events, including hurricanes, tornadoes, and tropical storms. It is separate from a standard homeowners policy.

How much does windstorm insurance cost in Texas?

Costs typically range from $1,600 to $2,400 per year for coastal properties. The average TWIA policy runs about $2,480 annually, though private market options may differ based on your property's specifics.

Does TWIA use credit scores to set premiums?

No. TWIA does not use credit scoring or territorial rating when calculating premiums. However, some private windstorm insurers may factor in credit history.

What is a WPI-8 certificate?

A WPI-8 certificate is an official document certifying that a property meets the Texas Department of Insurance windstorm building code requirements. It is typically required to obtain windstorm coverage in designated coastal areas.

Can I get windstorm insurance during hurricane season?

Windstorm insurance cannot be written when a named storm is actively in the Gulf of Mexico. It is best to secure coverage well before hurricane season begins on June 1.

Does windstorm insurance cover flood damage?

No. Flood damage requires a separate flood insurance policy. Windstorm coverage applies only to damage caused by wind and hail, not rising water or storm surge.

How can I lower my windstorm insurance premium?

You can lower costs by retrofitting your home to meet current building codes, choosing a higher deductible, maintaining your roof, and comparing quotes from both TWIA and private carriers through an independent insurance agent.

Is windstorm insurance required in Texas?

It is not legally mandated statewide, but mortgage lenders in coastal counties typically require it as a condition of loan approval. In practice, most Gulf Coast homeowners need it.

Protect Your Coastal Property Today

Do not wait until a storm is in the Gulf to think about windstorm coverage. Brad Spurgeon Insurance Agency has helped over 60,000 Texans find affordable windstorm, home, and flood insurance. As an independent agency in Texas City, TX, we compare rates from multiple carriers, including private windstorm options and TWIA, to find you the best protection at the lowest cost. Request your free windstorm insurance quote today or call us at (409) 945-4746.