Wind-Only Policy: Do You Need One With Your Hazard Insurance?

If you own property along the Texas Gulf Coast, there is a good chance your standard homeowners policy does not cover wind damage. Many carriers exclude wind and hail in coastal counties, leaving homeowners exposed to the very peril most likely to strike. Understanding whether you need a separate wind-only policy is essential to keeping your home and finances protected. Below, we walk you through the key factors, explain how exclusions work, and show you how to close the gap in your coverage.

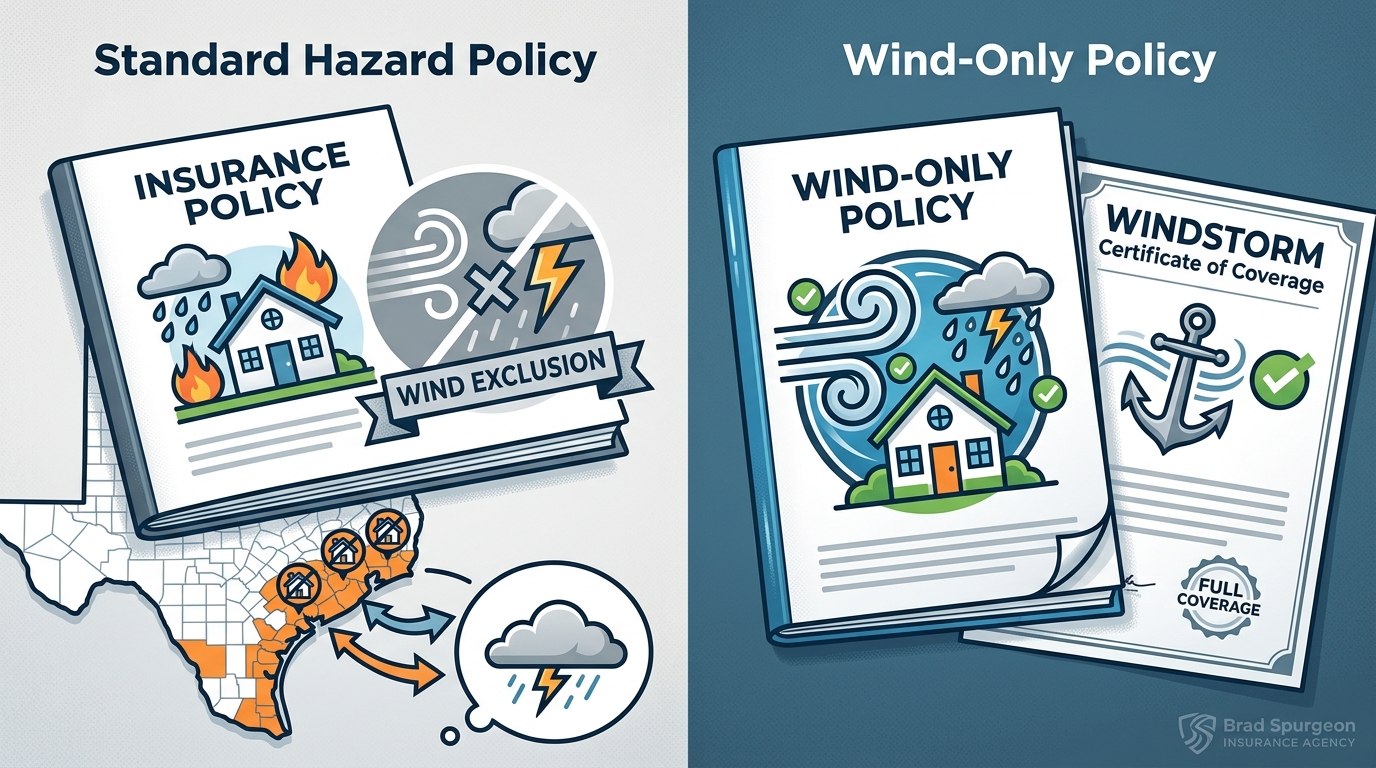

What Is a Wind-Only Policy?

A wind-only policy is a standalone insurance contract that covers property damage caused exclusively by wind and hail events. It exists because many standard homeowners (HO3) policies in coastal areas specifically exclude those perils. Windstorm insurance focuses on repairing physical damage from hailstorms, hurricanes, severe thunderstorms, tornadoes, and tropical storms.

The coverage typically extends to your dwelling, personal belongings, additional living expenses, and even lost rental income if the property becomes uninhabitable. If your hazard policy contains a wind exclusion endorsement, a wind-only policy is the standard way to restore that missing layer of protection.

How Wind Exclusions Work in Standard Hazard Insurance

Home insurance, also commonly called hazard insurance or homeowner's insurance, is a type of property insurance that covers a private residence. It bundles protections for the dwelling, personal property, liability, and loss of use. However, insurers operating in hurricane-prone regions often attach a wind and hail exclusion endorsement to the policy.

Reading Your Declarations Page

Your declarations page (or "dec page") lists every peril that is covered and excluded. Look for language such as "wind/hail excluded" or a reference to endorsement HO-300. If you see that language, wind damage is not part of your policy.

Why Carriers Exclude Wind

Insurers manage catastrophic risk by limiting exposure in high-loss coastal zones. After major hurricane seasons, many carriers pulled wind coverage from standard policies along the Gulf Coast, forcing homeowners to seek separate solutions.

Geographic Triggers Along the Texas Coast

The Texas Department of Insurance designates specific coastal territories where wind and hail coverage is commonly excluded from standard policies. These designated catastrophe areas include 14 first-tier coastal counties and portions of adjacent counties. Communities such as Texas City, Galveston Island, Tiki Island, Bayou Vista, League City, and Crystal Beach all fall within or near these zones.

If your property sits inside the designated territory, there is a strong probability you will need a separate wind-only policy. Properties outside these zones may still have wind included in their standard HO3, though this varies by carrier.

Step-by-Step Checklist to Determine Your Need

Follow these steps to find out whether your property requires a separate wind-only policy:

- Pull your current declarations page. Identify whether wind and hail are listed as covered perils or excluded.

- Confirm your property's location. Determine if you are within a designated catastrophe area using your county and ZIP code.

- Contact your homeowners carrier. Ask directly whether wind is included or excluded on your policy form.

- Obtain a WPI-8 certificate. A WPI-8 is a windstorm inspection certificate issued after a qualified inspector verifies your property meets the Texas Windstorm Insurance Association building code standards. Many lenders and insurers require it.

- Compare wind-only options. Request quotes from both TWIA and private windstorm carriers to evaluate price and coverage differences.

- Review your mortgage requirements. Most lenders in coastal zones require proof of windstorm coverage before closing or renewing a loan.

TWIA vs. Private Windstorm Coverage

The Texas Windstorm Insurance Association (TWIA) is a state-created insurer of last resort that provides wind and hail coverage in designated coastal areas. For two decades, TWIA was essentially the only option for Gulf Coast homeowners. Today, private market alternatives have emerged, often with competitive rates and broader terms.

| Feature | TWIA | Private Windstorm |

|---|---|---|

| Eligibility | Designated catastrophe areas only | Varies by carrier; often broader |

| WPI-8 Required | Yes | Sometimes waived |

| Replacement Cost Option | Limited | Often available |

| Deductible Structure | Percentage-based (1%-5% of dwelling value) | Flat dollar or percentage options |

| Claims Handling Speed | Can be slower after major storms | Typically faster with private adjusters |

| Bundling Discounts | No | Possible when paired with HO3 |

Brad Spurgeon Insurance Agency now offers windstorm coverage with multiple private companies alongside home policies that include wind, giving Texas Gulf Coast homeowners more choices than ever.

Cost Factors and Deductible Structures

A windstorm deductible is the amount you pay out of pocket before your wind-only policy begins to pay a claim. In Texas, these deductibles are often expressed as a percentage of dwelling coverage rather than a flat dollar amount.

Typical Premium Drivers

- Distance from the coastline

- Age and construction type of the home

- Roof shape, materials, and attachment method

- Presence of storm shutters or impact-resistant glass

- Your chosen deductible level

Saving on Premiums

Upgrading your roof to meet current building codes, installing hurricane straps, and choosing a higher deductible can all reduce your wind-only premium. Ask your agent about available insurance quotes to compare savings scenarios side by side.

Key Takeaways

- Standard hazard insurance in Texas coastal counties frequently excludes wind and hail damage.

- A wind-only policy is a standalone contract that fills this specific coverage gap.

- Properties in the 14 first-tier coastal counties almost always require separate windstorm coverage.

- Check your declarations page and confirm your property's designated catastrophe area status.

- TWIA remains the insurer of last resort, but private windstorm carriers now offer competitive alternatives.

- A WPI-8 inspection certificate is often required for wind-only coverage eligibility.

- Comparing multiple quotes from both TWIA and private markets can save hundreds of dollars annually.

Frequently Asked Questions

Does my standard homeowners policy cover hurricane wind damage in Texas?

In many coastal counties, no. Carriers routinely exclude wind and hail in designated catastrophe areas. You must verify by reading your declarations page or contacting your agent.

What is a WPI-8 certificate?

A WPI-8 is a windstorm inspection certificate confirming your property meets the Texas Department of Insurance building code standards for wind resistance. It is typically required by TWIA and some private carriers.

How do I know if my property is in a designated catastrophe area?

The Texas Department of Insurance publishes a list of eligible territories. Your county, ZIP code, or a quick call to a local insurance agent can confirm your status.

Can I get wind coverage included in my homeowners policy instead of buying a separate policy?

Some carriers now offer HO3 policies with wind and hail included, even in coastal zones. Brad Spurgeon Insurance Agency works with carriers that provide this option, which can simplify your coverage and sometimes reduce total cost.

What does TWIA stand for?

TWIA stands for the Texas Windstorm Insurance Association. It is a state-established insurer of last resort providing wind and hail coverage in designated coastal territories.

Is private windstorm insurance cheaper than TWIA?

It depends on your property, location, and risk profile. In many cases, private windstorm carriers offer competitive or lower premiums, broader replacement cost options, and faster claims service.

What is the typical deductible on a wind-only policy?

Deductibles commonly range from 1% to 5% of the dwelling coverage amount. For example, on a home insured for $250,000, a 2% wind deductible equals $5,000 out of pocket before the policy pays.

Do I need both flood insurance and windstorm insurance?

Yes, they cover entirely different perils. Flood insurance covers rising water damage, while windstorm insurance covers damage from wind-driven forces. Neither substitutes for the other.

Get a Free Wind Coverage Review

Not sure whether your current policy leaves you exposed to wind damage? Brad Spurgeon Insurance Agency has helped over 60,000 Texans secure the right combination of home, flood, and windstorm coverage. Request a free consultation today and let our team review your declarations page, confirm your coverage gaps, and compare quotes from TWIA and private windstorm carriers. Call (409) 945-4746 or visit our online quote page to get started.