Does Private Windstorm Insurance Cover Damage From Named Hurricanes and Tropical Storms?

If you live along the Texas Gulf Coast, one of the most important questions you can ask before hurricane season is whether your windstorm insurance actually covers damage from named hurricanes and tropical storms. The short answer is yes. Private windstorm insurance is designed to pay for wind-driven damage regardless of whether the event is a named hurricane, a tropical storm, or an unnamed thunderstorm. However, there are critical limits and exclusions every homeowner should understand before a storm makes landfall. Below, we break down exactly what is and is not covered so you can protect your home and family with confidence.

What Is Private Windstorm Insurance?

Private windstorm insurance is a specialty property and casualty policy that covers damage caused by wind or hail events. Unlike coverage obtained through the state-backed Texas Windstorm Insurance Association (TWIA), private policies are underwritten by commercial carriers that may offer more flexible terms and competitive pricing.

Along the Texas coast, standard homeowners policies frequently exclude wind and hail damage. That means homeowners in areas like Texas City, Galveston, and League City need a separate windstorm policy to stay protected. Brad Spurgeon Insurance Agency helps coastal homeowners find the right windstorm insurance coverage through trusted private carriers.

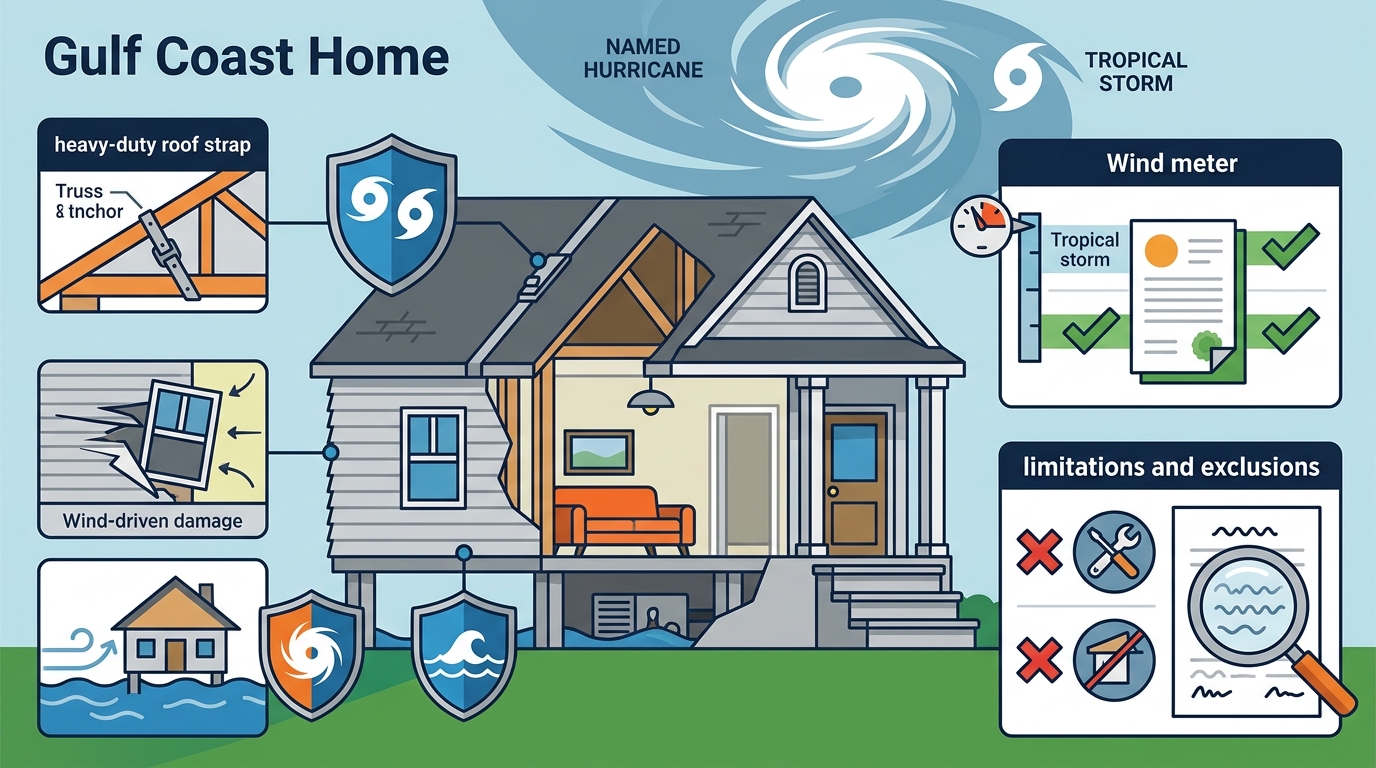

Does It Cover Named Hurricanes?

Yes. According to the Texas Department of Insurance, windstorm insurance pays to repair or rebuild your house if it is damaged by wind from a tornado, thunderstorm, or hurricane. A named hurricane is a wind event, so the wind-driven portion of that storm falls squarely within coverage.

A named hurricane is a tropical cyclone with sustained winds of 74 mph or greater that has been assigned a name by the National Hurricane Center. Whether the storm is called Hurricane Harvey or Hurricane Beryl, your private windstorm policy responds to the wind and hail damage it causes.

What the Policy Pays For

Windstorm insurance typically covers damage to your home's structure, roof, windows, and personal belongings caused by high winds. It may also cover additional living expenses if you are temporarily displaced from your home due to wind damage.

Tropical Storm Coverage Explained

A tropical storm is a cyclone with sustained winds between 39 and 73 mph. Private windstorm policies do not distinguish between named hurricanes and tropical storms when it comes to wind damage. If the wind from a tropical storm rips shingles from your roof or shatters a window, your policy applies.

This is especially relevant for Texas City homeowners because tropical storms can produce damaging wind gusts well above their sustained speed. Review your windstorm coverage details to confirm your limits and deductible structure before storm season begins.

Key Exclusions to Watch For

While private windstorm insurance covers wind-driven damage, it does not cover every type of destruction a hurricane brings. Understanding these exclusions is critical to avoiding costly surprises.

Flood and Storm Surge

Flood damage, even when caused by a hurricane, is not included in standard windstorm insurance. Storm surge is a separate peril classified as flooding. You need a dedicated flood insurance policy for that protection.

Pre-Existing Damage

If your property had damage before a covered storm, your windstorm policy will not pay for those existing issues. Carriers will inspect the property and may deny portions of a claim tied to pre-existing conditions.

| Peril | Covered by Windstorm? | Covered by Flood Insurance? |

|---|---|---|

| Hurricane-force winds | Yes | No |

| Tropical storm winds | Yes | No |

| Hail | Yes | No |

| Storm surge / rising water | No | Yes |

| Rain entering through wind-damaged opening | Yes | No |

| Inland flooding from rain | No | Yes |

TWIA vs. Private Windstorm Policies

The Texas Windstorm Insurance Association is a not-for-profit insurer of last resort serving designated coastal counties. TWIA policies cover wind and hail damage but pay claims on an actual cash value basis by default. A private windstorm policy, on the other hand, often includes replacement cost coverage as standard and may offer broader terms.

Private carriers can also be faster in claims processing and may bundle windstorm with your home insurance for simpler management. The average TWIA policy costs roughly $2,387 per year, though your rate depends on construction type, deductible, and coverage amount. Private options may be more competitive depending on your risk profile.

Who Qualifies for TWIA?

To obtain a TWIA policy, you must live in a designated coastal county, show proof of denial from at least one private insurer, and hold a valid windstorm certificate of compliance. If you can obtain private coverage, it is generally the preferred route. Contact Brad Spurgeon Insurance Agency to compare your options.

How to Prepare Before Hurricane Season

Preparation is key because windstorm policies cannot be written or modified once a storm enters the Gulf of Mexico. Here is what you should do now:

- Review your policy limits. Make sure your dwelling coverage reflects current rebuild costs. Request a free policy review to check for gaps.

- Verify your deductible. A deductible is the out-of-pocket amount you pay before your insurer covers the rest. Windstorm deductibles in Texas are often calculated as a percentage of dwelling coverage rather than a flat dollar amount.

- Secure flood insurance separately. There is typically a 30-day waiting period before a flood policy takes effect, so purchasing one at the last minute is not an option. Start with a flood insurance quote.

- Document your property. Photograph rooms, belongings, and exterior features to support any future claim.

Key Takeaways

- Private windstorm insurance covers wind damage from named hurricanes, tropical storms, tornadoes, and thunderstorms.

- Flood and storm surge damage are excluded from all windstorm policies and require a separate flood insurance policy.

- Coastal Texas homeowners typically need a standalone windstorm policy because standard home insurance excludes wind and hail.

- TWIA is the state-backed insurer of last resort; private carriers often offer more flexibility and replacement cost coverage.

- You cannot purchase or modify a windstorm policy once a hurricane enters the Gulf of Mexico.

- Windstorm deductibles in Texas are frequently percentage-based, not flat dollar amounts.

- Reviewing your coverage before June 1 each year helps you avoid dangerous gaps during Atlantic hurricane season.

Frequently Asked Questions

Does private windstorm insurance cover hurricanes in Texas?

Yes. Private windstorm insurance covers property damage caused by hurricane-force winds, including roof damage, broken windows, and structural harm. It does not cover flooding or storm surge caused by the same hurricane.

Is windstorm insurance the same as hurricane insurance?

They overlap significantly. Windstorm insurance covers all wind events, including hurricanes. Some people call it hurricane insurance, but a true hurricane brings both wind and water, and the water portion requires separate flood coverage.

Do I need windstorm insurance if I already have homeowners insurance?

If you live along the Texas coast, your homeowners policy likely excludes wind and hail damage. You will need a separate windstorm policy through a private carrier or TWIA to stay fully protected.

What is the difference between TWIA and private windstorm insurance?

TWIA is the state-created insurer of last resort for designated coastal counties. Private windstorm insurance comes from commercial carriers and may offer replacement cost coverage, faster claims, and competitive pricing.

Can I buy windstorm insurance during a hurricane?

No. Insurers, including TWIA, will not issue or modify windstorm policies once a tropical storm or hurricane enters the Gulf of Mexico. You must secure coverage well in advance.

Does windstorm insurance cover my fence or detached garage?

Most policies cover other structures on your property, such as fences, sheds, and detached garages, up to a specified percentage of your dwelling coverage. Review your declarations page for exact limits.

How much does private windstorm insurance cost in Texas?

Costs vary based on your home's location, age, construction type, and chosen coverage amount. The average TWIA policy runs about $2,387 per year, but private carriers may offer different pricing. Get a personalized windstorm insurance quote to compare.

Is windstorm insurance required by law in Texas?

No. Texas law does not mandate windstorm insurance. However, mortgage lenders in coastal counties typically require it as a condition of your loan.

Protect Your Home Before the Next Storm

Do not wait until a hurricane is spinning in the Gulf to find out you are unprotected. Brad Spurgeon Insurance Agency in Texas City, TX, specializes in private windstorm and flood insurance for Gulf Coast homeowners. Schedule your free consultation today and get the coverage you need before storm season arrives.