How to Qualify for Windstorm Insurance After Being Rejected by Multiple Providers

Getting turned down for windstorm insurance by multiple carriers can feel overwhelming, especially when you live along the Texas Gulf Coast where coverage is essential. The good news is that rejection does not mean you are out of options. Texas has programs and strategies specifically designed to help homeowners in high-risk coastal areas secure the wind and hail protection they need. In this guide, we walk you through every step you should take to qualify for a windstorm policy, from understanding why you were denied to leveraging the state's insurer of last resort and working with an experienced local agent.

Why Windstorm Insurance Applications Get Rejected

Windstorm insurance is a specialized policy that covers damage caused by wind and hail events such as hurricanes, tornadoes, and severe thunderstorms. In Texas, particularly along the 14 first-tier coastal counties, standard homeowners insurance policies typically exclude wind and hail damage. That exclusion forces homeowners to seek standalone windstorm coverage.

Common reasons for rejection include an older roof that does not meet current building codes, a missing windstorm inspection certificate, unrepaired storm damage, or a property located in an extremely high-risk flood zone without the required flood policy. Understanding the specific reason for your denial is the critical first step toward resolving the issue.

Understanding TWIA: Texas's Insurer of Last Resort

The Texas Windstorm Insurance Association (TWIA) is a not-for-profit insurance organization created by the Texas Legislature in 1971 after Hurricane Celia devastated Corpus Christi. TWIA provides wind and hail coverage to property owners in designated high-risk coastal areas who cannot obtain coverage through the standard insurance market. It is governed by Texas Insurance Code Chapter 2210.

A TWIA policy is intended to be a last resort. It covers damage from windstorms and hail but not other perils like fire, theft, or flooding. You should pair it with a traditional homeowners insurance policy and a separate flood insurance policy for comprehensive protection. A.M. Best rates TWIA's financial strength as A (Excellent), indicating strong ability to meet claims obligations.

Key Eligibility Requirements You Must Meet

To qualify for TWIA coverage, your property must satisfy several criteria established by the Texas Legislature. The table below summarizes each requirement and what it means for you.

| Requirement | Details |

|---|---|

| Location | Property must be in a designated catastrophe area (14 first-tier coastal counties or parts of Harris County east of Highway 146) |

| Private Market Denial | Applicant must have been denied coverage by at least one authorized insurer actively writing windstorm and hail coverage in the area |

| Building Code Certification | Property must hold a WPI-8 or WPI-8-E Certificate of Compliance from the Texas Department of Insurance (TDI) |

| Flood Insurance | Properties in flood zones V, VE, or V1-30 constructed or modified after September 1, 2009 must carry flood insurance |

| Insurable Condition | Property must be in good repair with no unrepaired damage or hazardous conditions |

Texas City falls within Galveston County, one of the designated first-tier counties, so location eligibility is typically straightforward for residents in this area. Understanding why windstorm insurance rates vary can also help you budget for the right coverage level.

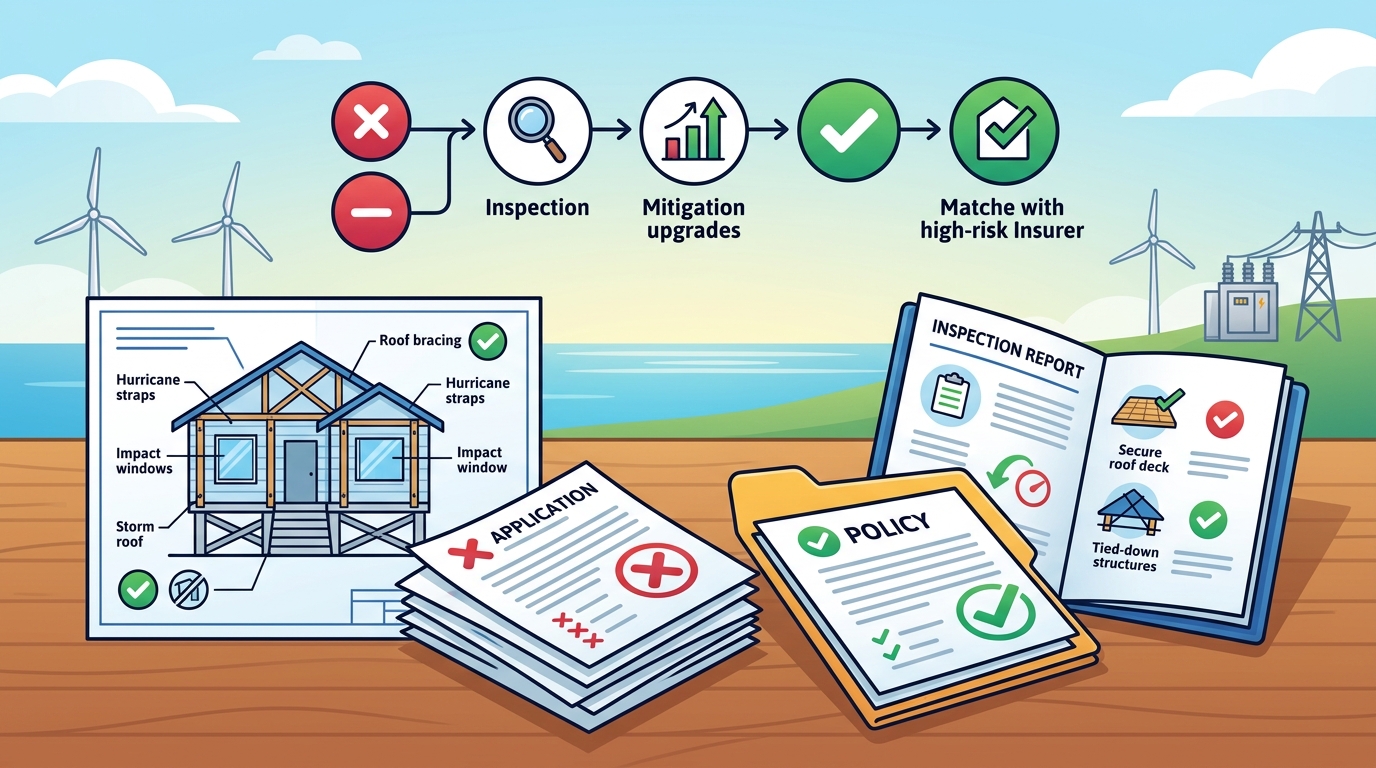

How to Obtain a WPI-8 Certificate of Compliance

A WPI-8 is the official document issued by the Texas Department of Insurance certifying that a structure meets the Texas Windstorm Building Code requirements. Without this certificate, TWIA lacks evidence that the structure conforms to applicable codes, and the property may be considered uninsurable.

When Is a WPI-8 Required?

Most properties built or modified after January 1, 1988 need a Windstorm Certificate of Compliance. Any new roof or re-roof in a TWIA-designated zone must pass a windstorm inspection and receive a WPI-8 certificate. As of June 1, 2020, all Certificates of Compliance are issued by TDI as part of its Windstorm Inspection Program.

How to Request an Inspection

Work with your contractor to request a TDI inspection during construction or roofing work. A qualified windstorm inspector, typically a Texas-licensed professional engineer or TDI-appointed inspector, will evaluate the structure at various stages. If your property passes, the inspector issues the WPI-8 form. The inspection itself is free.

What If You Are Buying an Existing Home?

Ask the previous owners for a copy of their certificate. You can also search for an existing WPI-8 on the TDI website. If no certificate exists, you may need to bring the property into compliance before obtaining coverage.

Getting Your Property Into Insurable Condition

Insurable condition is the standard TWIA uses to confirm a property is in good repair. TWIA regularly inspects properties as part of its underwriting process to verify rating accuracy, discover unrepaired damage, and identify hazardous conditions. Properties may be inspected physically or remotely using high-quality aerial imagery.

To improve your chances of qualifying, address these items before applying:

- Repair any existing roof damage, especially missing shingles or exposed decking

- Replace outdated roofing materials with impact-resistant options (Class 3 or Class 4 rated shingles can reduce storm damage claims by 60 to 80 percent)

- Secure loose siding, windows, and doors

- Install hurricane clips or straps connecting your roof to wall framing

- Remove hazardous conditions such as dead trees or unstable structures

Investing in these upgrades not only helps you qualify but can also lower your premiums. Learn more about how roof age impacts insurance costs and what improvements make the biggest difference.

Step-by-Step Application Process

Once your property meets all eligibility criteria, follow these steps to secure coverage:

- Document your private market denials. You need proof of rejection from at least one authorized insurer. If you were only offered coverage more limited than a TWIA policy, that also counts as a denial.

- Contact a licensed insurance agent. TWIA does not sell policies directly. You purchase coverage through any Texas-licensed property insurance agency. Brad Spurgeon Insurance Agency specializes in helping Texas City homeowners navigate this process.

- Gather your WPI-8 certificate. Provide the Certificate of Compliance to your agent for submission with the application.

- Secure flood insurance if required. If your property is in flood zone V, VE, or V1-30, obtain a flood insurance policy before applying.

- Submit the application. Your agent will compile property details including age, roof type, and construction materials and submit everything to TWIA underwriting.

- Complete the underwriting inspection. TWIA may conduct an in-person or remote inspection using aerial imagery.

- Review and accept the offer. Once approved, TWIA issues an offer of insurance. Choose your deductible (options include $100, $250, or 1% for residential policies) and pay to bind coverage.

Key Takeaways

- Being rejected by private insurers does not leave you without options. TWIA exists specifically as a last resort for coastal Texas homeowners.

- You must have at least one documented denial from a private insurer to qualify for TWIA coverage.

- A WPI-8 Certificate of Compliance from TDI is essential. Without it, your property may be considered uninsurable by TWIA.

- Properties must be in good repair with no unrepaired damage or hazardous conditions before TWIA will approve coverage.

- Impact-resistant roofing materials and hurricane-rated upgrades can both help you qualify and lower your premiums.

- TWIA covers wind and hail only. You still need separate home and flood insurance for full protection.

- Working with a local agent experienced in windstorm coverage simplifies the entire process.

Frequently Asked Questions

What is TWIA?

TWIA is the Texas Windstorm Insurance Association, a not-for-profit insurer created in 1971 by the Texas Legislature to provide wind and hail coverage to property owners in designated coastal areas who cannot find coverage in the private market.

What is a WPI-8 certificate?

A WPI-8 is the official Certificate of Compliance issued by the Texas Department of Insurance confirming that a structure meets the Texas Windstorm Building Code requirements. It is required for most properties seeking TWIA coverage.

How many denials do I need before I can apply to TWIA?

You need at least one denial from an authorized insurer that actively writes or renews windstorm and hail coverage in your designated area. Being offered only limited coverage that does not meet your needs also qualifies as a denial.

Does TWIA cover flood damage?

No. TWIA policies cover only wind and hail damage. Flood damage requires a separate flood insurance policy, either through the National Flood Insurance Program (NFIP) or a private insurer. Learn about your options on our flood insurance page.

What counties are eligible for TWIA coverage?

TWIA coverage is available in 14 first-tier coastal counties including Galveston, Brazoria, Chambers, Jefferson, Nueces, Cameron, and others, plus parts of Harris County east of Highway 146. Texas City is located in Galveston County and is fully eligible.

Can I get a WPI-8 for an existing home I am purchasing?

If the home already has a WPI-8 on file, you can obtain a copy from TDI's online database or from the previous owner. If no certificate exists, you may need to bring the property into building code compliance and schedule an inspection through TDI.

How much does TWIA coverage cost?

Premiums vary based on factors like property location, construction type, roof age, and chosen deductible. Newer roofs with higher wind ratings and impact-resistant materials typically qualify for lower premiums. Request a personalized windstorm insurance quote to get an accurate estimate.

Do I still need homeowners insurance if I have TWIA?

Yes. TWIA is not a replacement for standard homeowners insurance. It covers only wind and hail damage. You still need a homeowners policy for perils like fire, theft, and liability, plus a flood policy if you are in a flood-prone area.

Get Help From a Local Windstorm Insurance Specialist

Navigating windstorm insurance after multiple rejections is easier with an experienced local agent on your side. Brad Spurgeon Insurance Agency in Texas City, TX, specializes in windstorm, home, and flood insurance for Gulf Coast homeowners. We can help you understand your denials, prepare your property, and secure the coverage you need. Schedule your free consultation today and take the first step toward protecting your home.